Momentum & Growth continue to dominate

Diversified US Benchmarks: Winners & Losers YTD

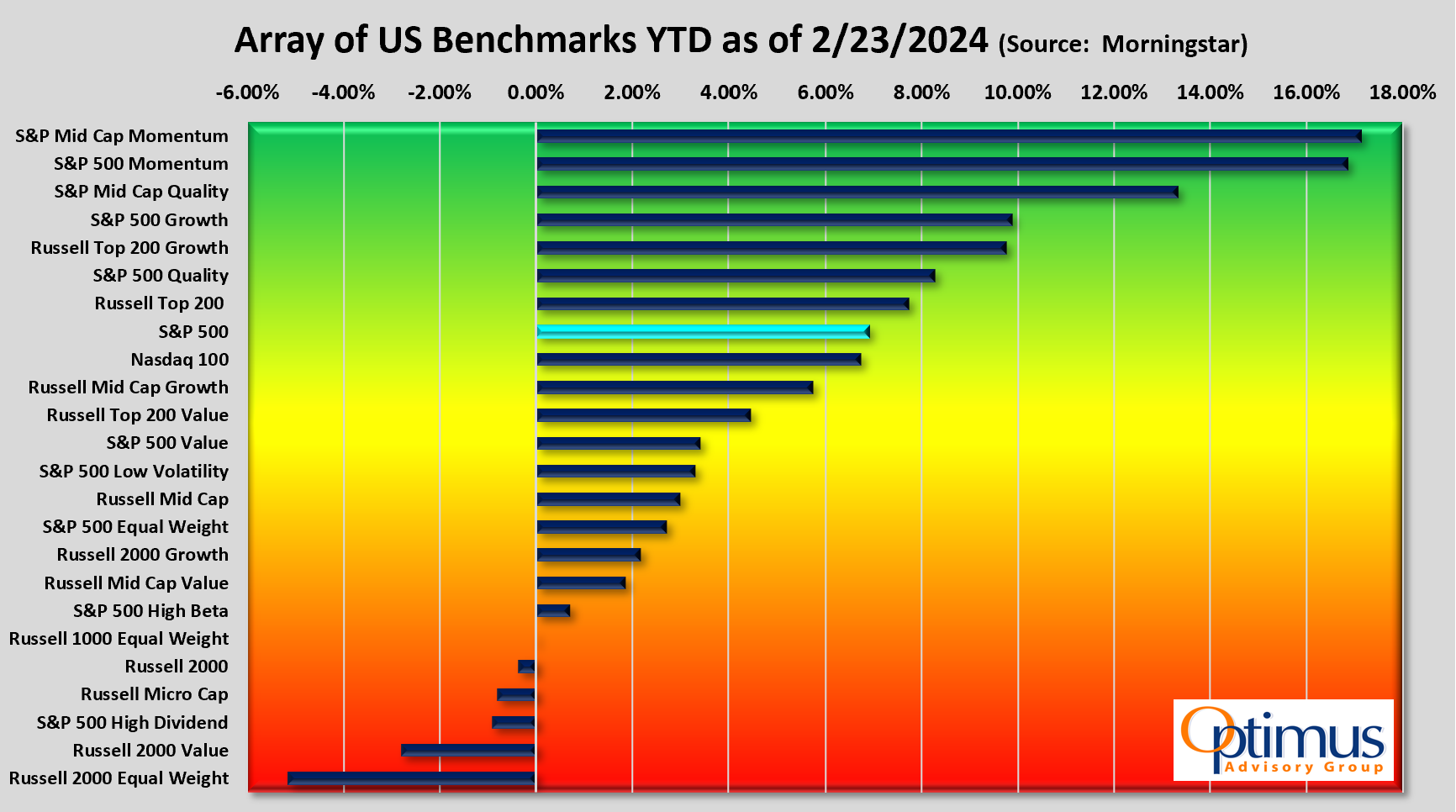

Much like the end of 2023, large cap growth continues to be strong in 2024. As of 2/23/2024, S&P 500 Growth is beating the S&P 500, 9.88% vs. 6.91%.

That being said, there are several other diversified benchmarks that are outpacing S&P 500 Growth.

YTD Winners:

Best – S&P Mid Cap Momentum: This S&P index is beating S&P 500 Growth by a huge margin (17.14% vs. 9.88%) and doing so while not relying on heavy Tech & Comm weightings (17.2% in T&C vs. 61.3% for S&P 500 Growth). Super Micro Computer, a provider of high-performance server technology services, is the largest holding followed by Decker Outdoor, which designs & sells casual and performance footwear/apparel, and Reliance, a diversified metal solutions provider. S&P Mid Cap Momentum has been a key holding for our Dynamic Equity and Equity Rotation models this year.

2nd Best – S&P 500 Momentum: This benchmark is right behind its mid cap cousin for YTD performance (16.85% vs. 9.88% S&P 500 Growth), but this index is heavily invested in Tech & Comm, with T&C holdings making up 40.09% of the benchmark (which is still much lower than S&P 500 growth at 61.3% and closer to the S&P 500’s 39.7% in T&C). Familiar names such as Meta Platforms (Facebook) and chip-maker NVIDIA make up 22.9% of the entire benchmark.

YTD Losers:

Small caps continue to struggle, as their large cap peers dominate the performance chart. The so-called “Magnificent 7” continue to suck all the oxygen out of the room and push large cap benchmarks to new all-time highs.

Worst – Russell 2000 Equal Weight: Instead of the usual cap-weighted indexing method, this benchmark divides its holdings equally. That way, no handful of stocks drive its performance. It also gives you a quick snapshot of just how the AVERAGE small cap stock is doing. In this case, they’re not doing well. The index is down -5.16% YTD.

2nd Worst – Russell 2000 Value: This index is down -2.80% YTD. While its objective is obviously to own small cap value stocks, there is no single stock that is greater than 0.5% of the benchmark, so it is very diversified. Unfortunately, being heavily invested in Financial Services (23.44%) and Industrials (12.76%) in this growth dominant market environment is not a great option.

Summary: We continue to see large cap growth and now even some mid cap growth areas of the market as the places to be in early 2024. Our equity strategies are tilting strongly in favor of large cap growth and large cap blend style boxes. We do continue to monitor the YTD gap between the S&P 500 (+6.91%) and the Russell 1000 Equal Weight (-.02%), as this was a theme for most of 2023 as well. We would like to see the strength in the market spread out to include most stocks, not just the mega large cap ones.